A.P. Moller Holding, the Maersk family’s investment vehicle, has agreed to buy Norway’s Ocean Yield from KKR, an acquisition that hands it a ship-leasing platform with interests in more than 70 vessels.

The purchase moves one of Europe’s larger maritime leasing books out of private equity and into permanent family capital. A different kind of owner, with a different clock.

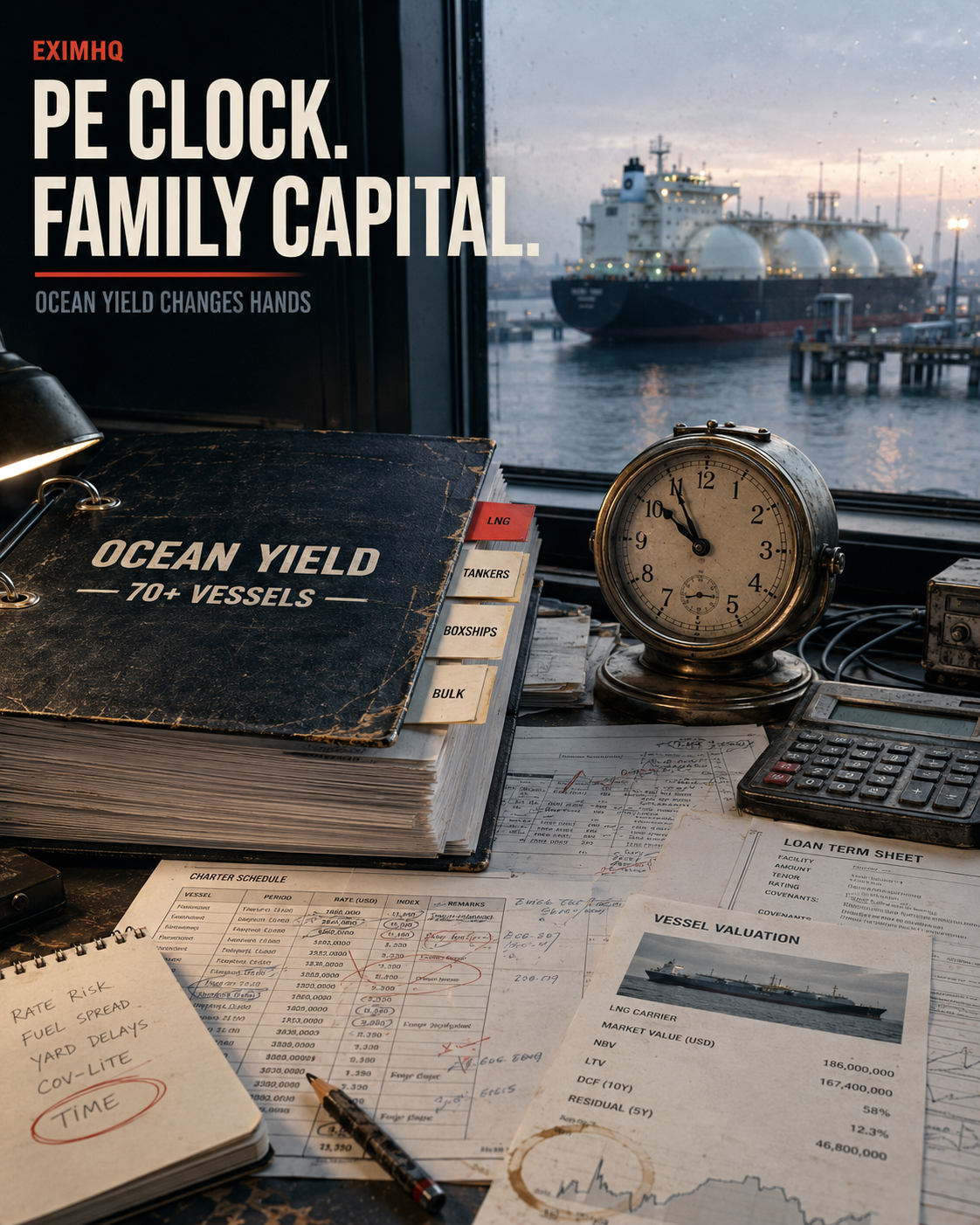

Ocean Yield’s fleet spans gas, tankers, boxships and dry bulk

Ocean Yield, headquartered in Oslo, holds interests in over 70 vessels across several core shipping sectors. The book runs from gas carriers and LNG carriers through crude, product and chemical tankers, container ships and dry bulk carriers. The largest single blocks outside gas are 12 crude oil tankers and 10 containerships, with dry bulk and other tonnage filling out the rest.

LNG carriers make up nearly half the platform

LNG carriers account for close to half of Ocean Yield’s investment, or 30 vessels. The company has kept building in energy: it recently extended a joint venture with Japan’s NYK to add four more LNG carriers, taking that JV to eight vessels, all chartered to Cheniere Energy. Fresh deliveries have gone on charter to Qatar Energy.

Ocean Yield’s chief executive, Andreas Røde, framed the platform around “long-duration, high-quality contracted cash flows” and a fleet built for the energy transition. Which is precisely the paper A.P. Moller Holding is paying for.

KKR exits after four years and more than $3 billion

KKR bought Ocean Yield in 2021, roughly nine years after the lessor was founded in 2012, and is now selling after putting more than $3 billion into the platform. The private equity firm says it scaled and diversified the book and steered the fleet toward more modern, lower-emission tonnage. KKR is not walking away entirely: it keeps its joint stake with Ocean Yield in CapeOmega Gas Transportation, which owns 10 of the LNG carriers.

ALSO READ:Konecranes buys Coapsa nuclear and port service units

A.P. Moller Holding keeps stacking maritime assets

A.P. Moller Holding, set up by the Maersk family in 2013 as the group’s investment arm, is the parent company of the A.P. Moller Group. Its maritime holdings already run from Maersk itself to Svitzer tugs, DOF offshore, Noble Drilling, [Maersk Tankers](EXIMHQ-INTERNAL: EximHQ profile of Maersk Tankers and the A.P. Moller maritime holdings) and Maersk Offshore Wind. Ocean Yield adds a dedicated leasing platform to that mix and deepens the family’s exposure to LNG.

The Ocean Yield acquisition is really a cost-of-capital play

For maritime asset-finance teams, the interesting number in this deal is not the fleet count but the buyer’s cost of capital. A leasing platform earns the spread between what it pays to fund a vessel and the charter rate it locks in. Lower the funding cost against the same contracted income and the whole book is worth more. Ocean Yield’s LNG carriers sit on multi-year charters to Cheniere Energy and Qatar Energy, contracted payment streams a permanent-capital holding company can borrow against cheaply and hold for years. A.P. Moller Holding is not really buying ships. It is buying a stream of contracted payments and a cheaper way to fund them.

A.P. Moller Holding did not assemble Svitzer, DOF, Noble Drilling, Maersk Tankers and Maersk Offshore Wind by buying once and stopping. The Maersk family vehicle tends to buy what funds are structurally forced to sell, and then it holds. Ocean Yield’s LNG paper is the kind of asset that stays on a book for a decade, not a fund’s five-year window, so the question worth watching is which maritime lessor coming off a private-equity clock next lands on the same buyer’s list.