Ten operators now control 57 percent of the VLCC fleet, up from under half a year ago, and rates sit at their highest since early 2020. Gibson, the shipbroker, calls the tanker market a hostage of geopolitics.

Venezuela, Hormuz, Ukraine, sanctions. It is also a control story, and the two are now braided together. A handful of owners hold more of the very large crude carrier (VLCC) tonnage than they did a year ago, and every geopolitical shock now lands on a fleet with no slack left to absorb it.

Venezuela’s reopening pulled 8% of the dark fleet back into daylight

The year began with a shock. On 3 January, a US operation captured Venezuelan President Maduro after a naval blockade and military buildup. What followed was sanctions relief, policy reform and foreign investment, and Venezuelan crude and dirty petroleum product (DPP) exports have since climbed back to a six-year high.

The tanker market consequence runs through a single mechanism. Venezuela accounted for 8 percent of dark fleet employment last year. When sanctioned barrels return to compliant trade, they come off the shadow ships and move onto mainstream tankers. Demand for mainstream tonnage rises without a single new barrel being pumped. That is a structural shift, not a price blip.

A regional earthquake this week leaves one question open. Gibson notes it is not yet clear whether Venezuelan production takes a hit.

Ten operators now hold 57 percent of the VLCC fleet

The consolidation story started in 2025. The VLCC market only began to feel it in the first months of 2026, when aggressive chartering pushed freight rates to levels last seen during the floating-storage scramble of early 2020.

Ten operators now control 57 percent of the VLCC fleet, against less than half a year ago. Scale gives them a lever on tonnage supply, and they are using it. The market stays volatile because a small group can now tighten or loosen the available ships at will.

The Hormuz closure broke the link between oil prices and freight rates

At the end of February, a US move triggered the closure of the Strait of Hormuz, the event the industry had feared and debated for decades. The strait shut, no one proved willing to pay the human and military cost of forcing it back open, and the oil market lost its anchor.

Tanker rates set records, both on paper and on the water. Physical oil prices hit record levels, and for a stretch freight rates stopped mattering at all. Then the market did what deep markets do. It absorbed the blow high pre-war inventories at sea and on land, an IEA-coordinated 400 million barrel emergency release, Saudi Arabia and the UAE diverting cargoes through pipelines that bypass Hormuz, and softer Asian demand all bought time. Barrels began slipping out of the strait again in coordination with the US military, the UAE and Oman.

This month, the US and Iran signed an interim peace deal. Hormuz reopened, transits are rising, and inventories have so far avoided running dry.

Iran, the UAE, and the cracks in OPEC discipline

The Iran deal carried a freight angle. Temporary sanctions relief opens the prospect of Iranian oil returning to mainstream tankers, even if UK, EU and UN measures may still block the lifting for now. The door is not open. It is no longer locked.

The 2025 worry was an oversupplied market and an OPEC forced to cut. Hormuz erased that argument, and it did not survive the reopening intact either. The UAE wants out of its quota and is acting like it, with crude exports averaging a record 3.6 million barrels per day so far this month. Iraq, Gibson reports, may be reconsidering its own place in the group.

The logic is plain. Once one member breaks a quota and is rewarded with record exports, the rest face a single choice: hold the line alone and lose share, or follow and keep it. Iraq’s reported second thoughts are the first sign of the follow.

Russia is being squeezed by drones, not sanctions packages

Russia started the crisis ahead. Higher prices helped, and US sanctions waivers let India temporarily raise Russian imports alongside its first Iranian cargo since 2019. The EU answered with its 20th sanctions package.

But the real pressure came from the battlefield. Ukraine’s long-range drones have hit Russian refineries with growing effect, and the fuel shortages that followed pushed Russian clean petroleum product (CPP) exports to a record low. Crude exports went the other way, hitting a record high in May as idled refineries forced unrefined barrels out the door. Twenty sanctions packages moved the price. The drones moved the refineries. With prices softening and product exports under strain, the pressure on Moscow keeps building, even if an end to the war is still hard to picture.

Owners are ordering into the chaos

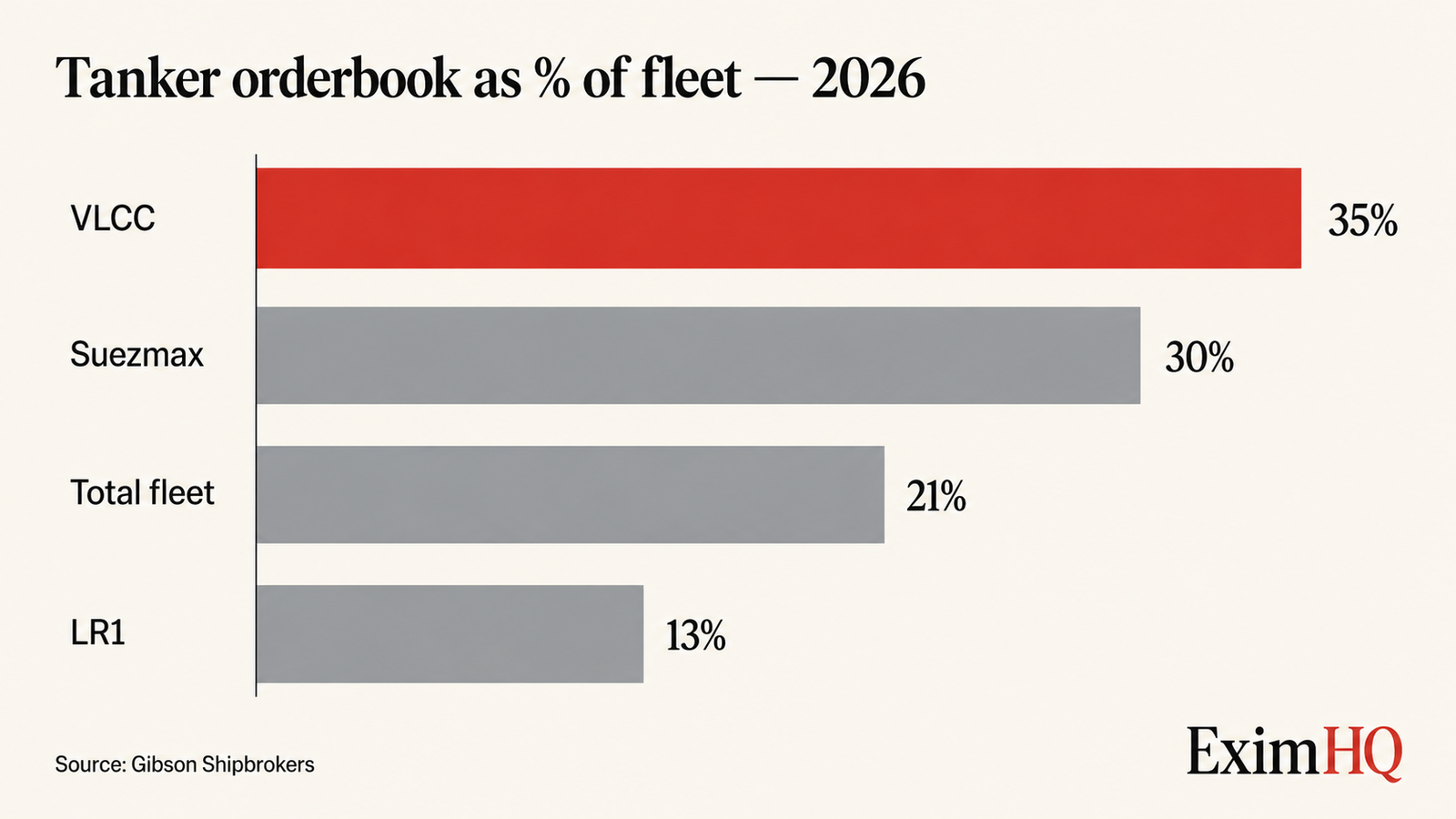

None of this has slowed the order pipeline. Tanker orders above 25,000 dwt have already passed last year’s full-year total, and 2026 is already a record year for VLCC orders with half the year still to run. The total orderbook stands at 21 percent, from 35 percent for VLCCs down to 13 percent for LR1s, with Suezmax orders climbing to 30 percent.

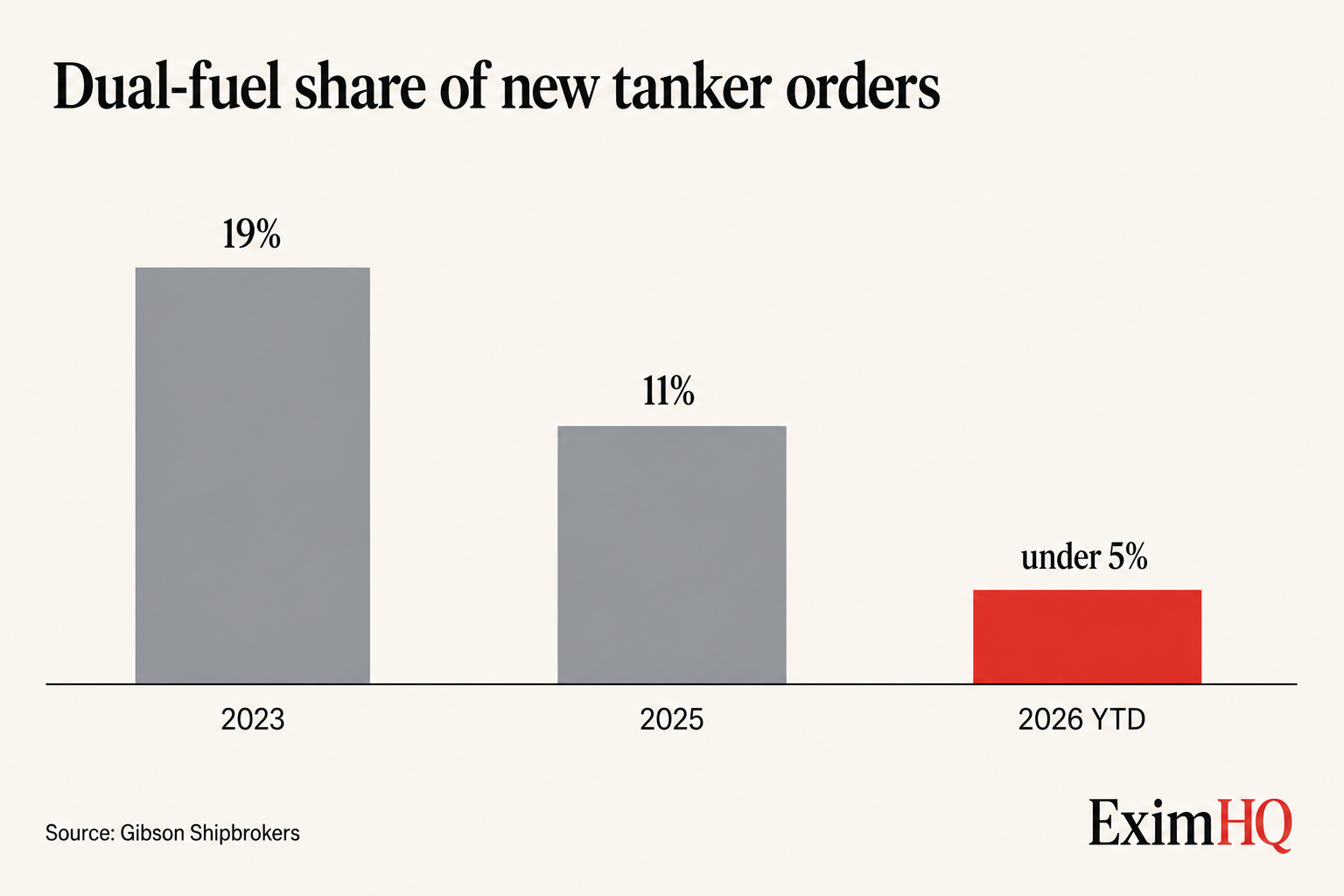

The fuel transition, meanwhile, has stalled. Under 5 percent of this year’s tanker orders are dual-fuel or dual-fuel-ready, against 11 percent last year and 19 percent in 2023. Part of that is regulatory limbo. The US and its allies blocked the IMO Net Zero Framework (NZF) last December, and even an amended version faces the threat of US sanctions on anyone enforcing it against US interests. Best case, it would not bind until 2029, and Gibson rates even that as unlikely.

ALSO READ:Kongsberg Maritime leads EU wind propulsion project

So owners are building conventional steel with no transition penalty in sight. Deliveries from the yards hit a 16-year high over the last six months, weighted toward Aframax and LR2 crude and product carriers and MRs. Scrapping all but stopped: eight tankers sold for demolition, against 20 in the same window of 2025.

The orders placed this year cannot be unplaced. Record VLCC tonnage delivers into 2027 and beyond, into a market currently held up by a one time inventory rebuild and a strait that has only just reopened. Scrapping is near zero, so nothing is leaving to make room.

The one thing standing between that incoming steel and an oversupplied market is the discipline of ten operators who hold 57 percent of the fleet. Concentration can hold a market up for a year or two. A record orderbook meeting a fading crisis usually wins in the end.